Choosing the lowest interest rate on a car loan might actually be the most expensive way to put a new vehicle in your driveway this year. While 52% of Australians still source a loan directly from a lender, many are realising that paying for a car with after-tax income is a missed opportunity for significant savings. When weighing up a novated lease vs car loan in 2026, the real winner isn’t found on a bank’s rate sheet but in the reduction of your taxable income.

It’s understandable if you feel frustrated by high monthly repayments or confused by the shifting FBT and GST rules. You want a clear path to lower your taxable income and simplify your car’s admin without the anxiety of a looming balloon payment. This article provides the definitive financial breakdown between salary packaging and traditional car loans to help you maximise your tax savings and cash flow. We will compare the total cost of ownership, explain how the EV FBT exemption can save you up to $12,000 annually, and show you how to secure the most competitive quote in the current market.

Key Takeaways

- Grasp the structural mechanics of a tripartite salary packaging agreement compared to a standard two-party finance contract.

- Maximise your monthly cash flow by applying GST savings to both the vehicle’s purchase price and your bundled running costs.

- Evaluate the definitive cost difference between a novated lease vs car loan for electric vehicles under the 2026 FBT exemption thresholds.

- Learn how to manage lease portability to ensure your tax-effective arrangement remains intact even if you change employers.

- Use a pragmatic decision matrix to determine if salary packaging or traditional finance best suits your specific financial profile.

The Fundamental Difference: Salary Packaging vs Private Finance

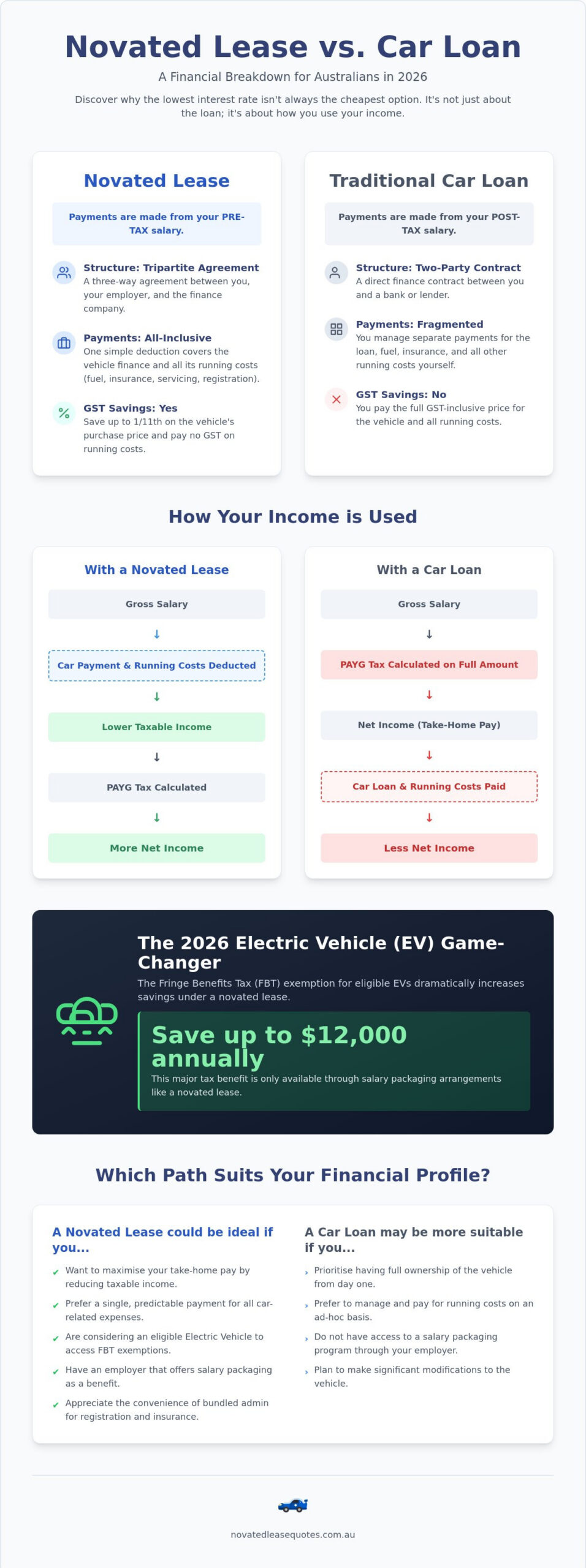

Most drivers view car finance as a straightforward debt to be repaid. However, the debate of novated lease vs car loan isn’t just about interest rates; it’s about how you use your gross income. A car loan is a private arrangement. You borrow money, buy the car, and then manage insurance, fuel, and rego from what’s left of your pay. A novated lease flips this model by integrating your vehicle into your employment contract, shifting the car from a personal expense to a structured tax benefit.

The primary distinction lies in how the money leaves your pocket. With a lease, your repayments are “all-inclusive,” covering the finance and all running costs in a single deduction. With a loan, those costs are fragmented. You pay the bank for the car, the petrol station for fuel, and the government for registration, all using money that has already been taxed. This creates a psychological and financial gap between the two options that goes far beyond the monthly sticker price.

How a Novated Lease Works in 2026

A novated lease is a tripartite agreement. It involves you, your employer, and a financier. For a neutral breakdown of this structure, you can read more about what is a novated lease and how it functions within Australian tax law. The “novation” refers to the transfer of the lease obligations to your employer. They pay the lease and running costs on your behalf using a combination of pre-tax and post-tax salary.

This salary sacrifice mechanism is the engine of your savings. By reducing your taxable income, you effectively pay less PAYG tax. It’s a common misconception that you’re restricted to a “company car” or a limited fleet. In 2026, you choose the car you want, from any dealer, and keep the flexibility to take the arrangement with you if you change jobs. Most Australian employers now offer this as a standard benefit because it’s a cost-neutral way to provide you with a significant pay rise in real terms.

The Mechanics of a Traditional Car Loan

In contrast, a car loan is a simple two-party contract. You deal directly with a bank or lender to borrow a lump sum. Once the funds are cleared, you have total ownership of the asset from day one, though the lender usually holds the car as security until the final cent is paid. This is the traditional path most Australians are familiar with, but it carries hidden inefficiencies.

The biggest hurdle with a loan is the “after-tax” trap. Every dollar you spend on the car has already been taxed at your highest marginal rate. You also have to manage every expense manually. When the registration is due or the tyres need replacing, that money comes straight out of your bank account. There’s no GST saving on the purchase price or the fuel, and no reduction in your annual tax bill. It’s a manual, fragmented way to manage what is often a household’s second-largest expense.

Financial Comparison: Tax Savings, GST, and Interest Rates

Interest rates are often the first thing people look at, but focusing solely on the “percentage” is a mistake. When comparing a novated lease vs car loan, the interest rate is just one variable in a much larger equation. A car loan with a 7.65% interest rate might seem cheaper than a lease with a slightly higher internal rate, but this narrow view ignores the massive tax offsets. You need to look at the “net position.” This is the actual cash remaining in your bank account after all car-related expenses are paid, rather than just the cost of the debt.

A major part of this equation is the GST. When you take out a car loan, you pay the full GST-inclusive price of the vehicle. However, under a novated lease, the financier can usually claim the GST back on the purchase price, effectively reducing the amount you need to finance by up to 1/11th. For a vehicle priced near the 2026-27 luxury car tax threshold of $80,809, this upfront saving is substantial. This cost comparison between leases and loans highlights how these immediate savings often outweigh interest rate differences over the life of the term.

The GST Advantage You Can’t Get with a Loan

Leasing companies act as the primary purchaser, allowing them to claim the GST on the vehicle’s price and pass that saving directly to you. This benefit also extends to your ongoing running costs. Every time you pay for fuel, servicing, or tyres through your lease, you aren’t paying the 10% GST. With a car loan, you pay the retail price for every litre of fuel using money that has already been taxed at your marginal rate. It’s a double hit to your wallet that most private borrowers simply accept as the cost of driving, despite the 2026 GST cap for luxury vehicles still allowing for significant credits on most popular models.

Pre-Tax vs After-Tax: The Real Cost of Ownership

Consider the impact on your take-home pay. If you spend $1,000 of your gross salary on a lease, that deduction happens before the taxman takes his share. If you’re in a common tax bracket, that $1,000 deduction might only reduce your actual take-home pay by around $630. Conversely, to pay a $1,000 monthly car loan bill, you actually need to earn significantly more in gross salary to cover the tax first.

The difference is stark. One option uses your pre-tax dollars to fund your lifestyle, while the other forces you to use after-tax dollars for the exact same asset. To see how these numbers apply to your specific salary and vehicle choice, you can use a novated lease calculator to model your potential savings. Finding the right fit for your budget starts with seeing the full financial picture, which is why many savvy drivers now compare tailored quotes before committing to a bank loan.

The 2026 EV Factor: Why Electric Vehicles Change the Game

Electric vehicles have completely rewritten the rules of vehicle finance. While earlier sections explored the general benefits of salary packaging, the 2026 landscape makes a traditional car loan for an electric vehicle almost impossible to justify financially. The difference in a novated lease vs car loan for an EV is no longer just a few hundred dollars; it’s a gap of thousands. This is primarily because the federal government’s FBT exemption for eligible electric vehicles remains the single most powerful tax break available to Australian employees.

Choosing a private loan for an EV means you’re voluntarily opting out of a massive government incentive. In 2026, the financial advantage of leasing an electric car is so significant that it often makes a $70,000 EV cheaper to run than a $45,000 petrol car. This shift is driven by the way the Australian Taxation Office (ATO) treats “green” fringe benefits, allowing you to pay for the car and its power using money that hasn’t been touched by the taxman.

Fringe Benefits Tax (FBT) Explained for 2026

Fringe Benefits Tax is normally a 47% levy applied to benefits provided by an employer in place of salary. For a standard petrol car, this tax usually offsets some of the salary sacrifice benefits. However, for 2026, eligible battery electric vehicles (BEVs) priced below the fuel-efficient Luxury Car Tax threshold of $91,661 are completely exempt from FBT. This exemption is confirmed to continue until March 31, 2027.

It’s vital to remember that plug-in hybrids (PHEVs) are no longer eligible for this exemption if the lease arrangement began after April 1, 2025. For a pure EV, this “Zero FBT” rule translates to an annual saving of between $6,000 and $12,000 depending on your income. When you use a car loan, you lose this entire benefit. You’re effectively paying a “tax penalty” for the privilege of owning the debt privately rather than packaging it through your payroll.

Bundling EV Running Costs

Beyond the purchase price, a lease simplifies the unique costs of EV ownership. You can package charging costs, specialised EV insurance, and high-performance tyres into your pre-tax deduction. Some providers even allow you to include the cost of a home charging station in the initial lease package. This creates a seamless experience where your only responsibility is driving, without the need to manage multiple separate bills.

Managing these costs with a private loan is far more complex. You’d have to track electricity usage for business claims and pay for expensive EV insurance from your net income. There’s also the matter of the residual value. The ATO sets mandatory minimum residual values, such as 46.88% for a three-year lease. In the 2026 market, these set percentages provide a structured exit strategy. They help you manage the resale risks associated with rapidly evolving battery technology, whereas a loan leaves you entirely at the mercy of the used car market with no tax-effective way to clear the balance.

Practical Considerations: Flexibility, Job Security, and Ownership

While the tax benefits are compelling, many drivers hesitate when weighing up a novated lease vs car loan due to concerns about employment flexibility. The most common question is what happens if you leave your job. It’s a valid worry, but the reality of the 2026 workforce is that these arrangements are designed to be portable. Unlike a company fleet car that you must return, a novated lease is your personal agreement that simply uses your employer as a payment gateway.

In contrast, a car loan offers complete independence from your workplace. If you change jobs, your loan remains exactly the same. However, you also remain responsible for paying every cent of the interest and running costs from your after-tax salary, regardless of your career moves. The choice between the two often comes down to whether you prefer the security of a fixed debt or the ongoing tax optimisation of a packaged benefit.

Job Changes and Lease Portability

If you move to a new employer, you can usually “re-novate” the lease. This involves your new company taking over the pre-tax payment obligations. Because salary packaging is now a standard part of Australian remuneration, most payroll departments handle these transitions seamlessly. If you find yourself between jobs, you simply transition to making the payments directly to the financier using your own funds until your next role begins.

During this transition, you lose the tax-free status of the payments, but the underlying contract doesn’t change. This makes the lease surprisingly resilient. You can find more detail on how these transitions work in the complete novated lease process, which covers the administrative steps for employees. A car loan is simpler in this regard, but it lacks the mechanism to ever turn your car into a tax-deductible asset.

The Residual Value (Balloon Payment) Reality

A key structural difference is how the debt is cleared. A car loan is typically designed to reach a $0 balance at the end of the term. A novated lease, however, must include an ATO-mandated residual value. This is a final lump sum payment required to take full ownership of the vehicle. For a three-year lease, this residual is set at 46.88% of the purchase price. For a five-year term, it drops to 28.13%.

This residual isn’t a hidden fee; it’s the reason your monthly repayments are so much lower than a car loan. At the end of the term, you have three primary choices:

- Pay the residual and own the car outright.

- Refinance the residual into a new lease term.

- Sell the car, use the proceeds to clear the residual, and keep any tax-free profit.

In 2026, we’ve seen a surge in used car novated leases. This allows drivers to apply these same tax-effective structures to high-quality second-hand vehicles, avoiding the sharpest part of the depreciation curve. Whether you choose new or used, the goal remains the same: maximising your net position. To see which structure fits your current career path, you should compare novated lease quotes against your best bank offer today.

Decision Matrix: Should You Choose a Lease or a Loan?

Decisions in the automotive finance market are rarely one-size-fits-all. While the data suggests that a novated lease is the superior financial engine for most Australian professionals, specific circumstances might still favour a traditional bank facility. The debate of novated lease vs car loan effectively ends when you align your personal tax position with your long-term vehicle usage. It’s about choosing the tool that preserves your cash flow while building the most value over time.

The 2026 landscape has made this choice clearer than ever. With interest rates for private loans remaining high and government incentives for electric vehicles reaching their peak, the “status quo” of bank finance is being challenged. To make the right call, you must look past the monthly repayment and evaluate the impact on your annual tax return and your daily administrative burden.

Choose a Novated Lease If…

Salary packaging is designed for efficiency. If your goal is to pay for your car, fuel, and charging with pre-tax dollars, this is the logical path. It’s particularly effective if you fall into a middle-to-high tax bracket where the PAYG savings are most pronounced. You should prioritise a lease if:

- You are considering an EV to take full advantage of the current FBT exemptions.

- You value a “set and forget” approach where registration, insurance, and servicing are managed through a single, automated payroll deduction.

- You want to avoid paying GST on the vehicle’s purchase price and ongoing running costs.

- You prefer the flexibility to upgrade your vehicle every three to five years without the hassle of private sales.

Choose a Car Loan If…

Traditional finance still has a place for certain types of buyers. While it lacks the tax-optimisation features of a lease, it offers a different kind of simplicity. A car loan might be your best option if:

- Your employer doesn’t offer salary packaging as a benefit, which is rare in 2026 but still occurs in some small businesses.

- You have a very low taxable income where the reduction in PAYG tax offers minimal financial gain.

- You plan to keep the car for a decade or longer and want to reach a $0 debt balance by the end of a five-year term without a residual payment.

- You prefer to manage all car-related admin and payments manually through your own bank account.

Regardless of which path you lean toward, the most critical step is to avoid the “first-offer trap.” Interest rates and management fees vary significantly between providers. Finding the best deal requires transparency and a side-by-side analysis of the total cost of ownership. You can start by using a novated lease calculator to model your specific salary against different vehicle models. Once you have your baseline, the most effective way to ensure you’re winning the novated lease vs car loan battle is to use a quote comparison service. This empowers you with multiple data points, ensuring you secure the most competitive terms available in the 2026 market.

Optimise Your Vehicle Finance for 2026

Evaluating the choice between a novated lease vs car loan requires looking beyond the interest rate to see the total impact on your taxable income. By leveraging pre-tax salary packaging and GST credits, you can significantly lower the cost of ownership compared to traditional bank finance. This is particularly relevant for electric vehicles, where the current FBT exemptions offer a unique window for substantial annual savings that a private loan simply cannot match.

To make an informed decision, you need data tailored to your specific salary and vehicle choice. We provide an independent and objective comparison with access to Australia’s leading leasing specialists and real-time tax saving calculations. Compare competitive novated lease quotes now and discover exactly how much you can improve your monthly cash flow. Take control of your car finance and ensure you aren’t paying more than you need to for your next vehicle.

Frequently Asked Questions

Is a novated lease worth it for someone on an average salary?

Yes, it’s often worth it because the tax savings apply regardless of your income level, though higher earners save more. For an average Australian earner, the ability to pay for fuel and servicing from pre-tax income reduces your taxable salary, which can help keep you in a lower tax bracket. When comparing a novated lease vs car loan, the average worker often sees a noticeable increase in their fortnightly take-home pay.

Can I get a novated lease on a used car in 2026?

You can certainly lease a used car in 2026, provided it meets the financier’s age and condition criteria. Most providers require the vehicle to be less than 10 or 12 years old by the end of the lease term. This has become a popular way to avoid the initial depreciation of a new vehicle while still accessing the GST savings on running costs and the tax-effective payment structure.

How do interest rates on novated leases compare to bank car loans?

Interest rates on leases are often slightly higher than the lowest bank rates, but focusing on the rate alone is misleading. The tax benefits and GST savings on the purchase price usually result in a lower total cost of ownership than a standard bank loan. It’s essential to look at the “net position” rather than just the percentage on the contract to see the true financial outcome of a novated lease vs car loan.

What happens to my novated lease if I am made redundant?

If you are made redundant, the lease “de-novates” and becomes a personal obligation. You’ll need to make the monthly payments from your own bank account using after-tax funds until you secure new employment. Once you start a new role, your new employer can usually take over the arrangement, allowing you to resume the salary packaging benefits and the convenience of automated deductions.

Do I still own the car at the end of a novated lease?

You gain full ownership of the vehicle once you have paid the ATO-mandated residual value at the end of the term. During the lease, the financier technically owns the car, but you have full use of it as if it were your own. After the final payment is cleared, the title is transferred into your name, or you can choose to trade the vehicle in for a new model.

Can I trade in my current car to start a novated lease?

You generally cannot trade in a car directly to a leasing company as you would with a dealership. Instead, you should sell your current vehicle privately or to a dealer and use those funds as you see fit. Because a lease is a salary packaging arrangement, it functions differently from a standard retail purchase, requiring a clean start with the new vehicle’s finance and running cost budget.

Is insurance included in a novated lease quote?

Comprehensive insurance is standard in a novated lease quote and is bundled into your single monthly deduction. This means you pay for your premiums using pre-tax dollars, effectively making the insurance cheaper than if you paid for it privately. You also retain the flexibility to choose your own insurer or use the provider’s preferred partner, ensuring you have the right level of cover for your needs.

Can I use a novated lease for a car I already own?

You can use a “sale and leaseback” arrangement to package a car you already own. The leasing company buys the car from you at its current market value, giving you a lump sum of cash, and then leases it back to you through your employer. This allows you to access the tax benefits of a novated lease vs car loan without having to go out and buy a brand-new vehicle.