Did you know that the FBT exemption for eligible electric vehicles can save you between $8,000 and $15,000 every year? It is a significant financial win, yet many professionals hesitate because the setup often feels like a logistical hurdle. You likely understand that salary packaging offers benefits, but the actual novated lease process for employees can seem daunting when you are faced with payroll questions or complex tax calculations.

We understand that you want the tax savings without the administrative headache. You might worry about your employer’s reaction or what happens if you change jobs, but these obstacles are easily managed with the right information. This guide promises to simplify the journey, giving you the confidence to secure your next vehicle while keeping your take-home pay as high as possible.

We will walk you through the entire roadmap, from comparing initial quotes and understanding the 2026 GST credits to finalising your agreement. You will learn exactly how to present this to your payroll team and how to maximise your savings using the latest ATO thresholds.

Key Takeaways

- Understand how the three-way agreement between you, your employer, and the financier unlocks significant tax advantages.

- Learn the exact novated lease process for employees to move from a calculator estimate to a final signed agreement.

- Discover how to reduce your vehicle purchase price by 10% through GST exemptions and lower your taxable income.

- See how fully maintained leases simplify ownership by bundling fuel, tyres, and servicing into a single payment.

- Find out why comparing multiple quotes is the smartest way to avoid hidden fees and secure competitive rates.

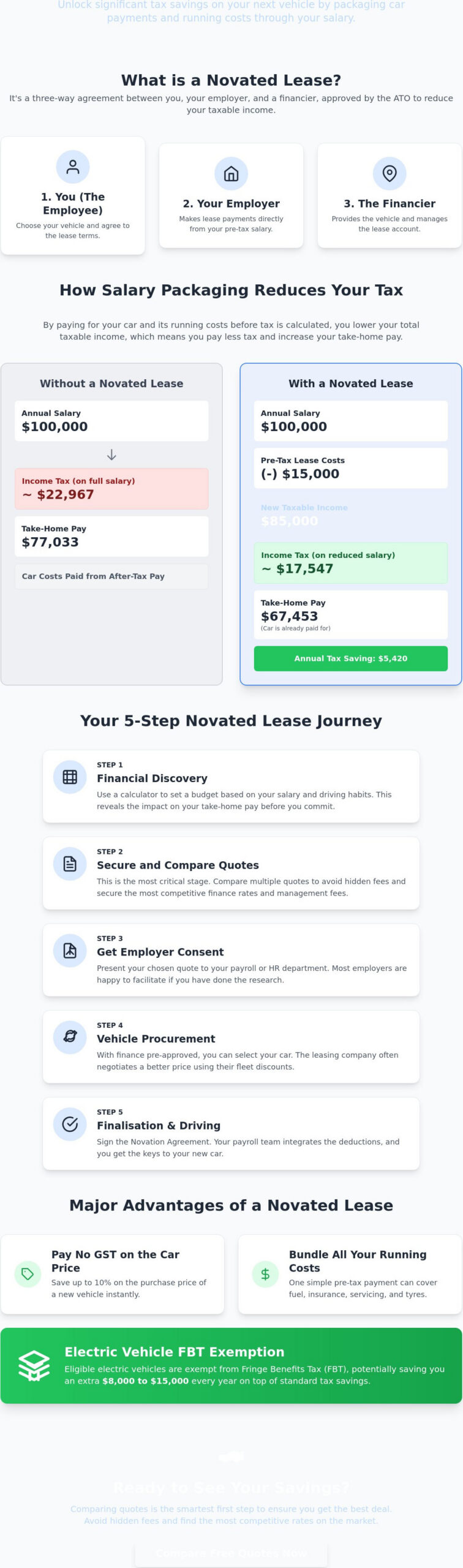

What is a Novated Lease? Understanding the Three-Way Agreement

A novated lease is a unique Australian financial arrangement that allows you to pay for a vehicle and its running costs using a combination of your pre-tax and post-tax salary. Unlike a standard car loan where you manage repayments from your bank account after tax has been taken out, this method integrates your car expenses directly into your payroll. Understanding the novated lease process for employees starts with recognising that this isn’t just a loan; it’s a strategic tax benefit sanctioned by the Australian Taxation Office (ATO).

The structure relies on a “three-way” partnership. You choose the vehicle and the financier, but your employer steps in to facilitate the payments. This relationship is formalised through a specific document known as a Novation Agreement. This legal instrument transfers the obligation of the lease payments from you to your employer for as long as you remain with the company. If you decide to move to a new job, the lease is “de-novated,” and the responsibility returns to you until you potentially organise a new agreement with your next employer.

For a deeper look at the historical and legal definitions, you can explore more about What is a Novated Lease? and its role in the Australian workforce. This structure is fundamentally different from a chattel mortgage or a consumer loan because it allows for the “salary packaging” of running costs like petrol, insurance, and servicing, which are usually paid for with after-tax dollars.

The Core Mechanism: How Salary Packaging Works

The primary goal of the novated lease process for employees is to reduce your taxable income. When your employer makes lease payments from your pre-tax salary, your total reportable income drops. For example, if you earn $100,000 and your lease costs $15,000 per year, you are only taxed on $85,000. This shift can often move you into a lower tax bracket, increasing your take-home pay by hundreds of dollars each month.

The ATO views this arrangement as a fringe benefit. While most fringe benefits attract a Fringe Benefits Tax (FBT) of 47% as of the 2026/27 financial year, many employees use the Employee Contribution Method (ECM) to offset this. By paying a portion of the running costs from post-tax income, you can reduce the FBT liability to zero. Additionally, with the current 2026 incentives, eligible electric vehicles remain FBT-exempt, making them the most efficient choice for many professionals.

Who is Eligible for a Novated Lease?

Your employer must also be willing to participate in salary packaging. Most medium-to-large Australian businesses already have these systems in place, but smaller firms may need to be guided through the setup. For organisations that are also looking to build a professional brand image alongside employee perks, sourcing high-quality custom clothing from RAW Merch is another popular way to invest in team culture.

Your personal financial standing also plays a role. Just like any other finance product, providers will assess your credit score and current debt-to-income ratio. Even though the payments come from your salary, the finance company needs to ensure you can comfortably meet the obligations over the three to five-year term of the lease.

The Step-by-Step Novated Lease Process for Employees

The novated lease process for employees is a logical sequence of events that moves from initial curiosity to driving a tax-optimised vehicle. While some providers suggest it is a single-step affair, a successful setup requires five distinct stages to ensure you maximise your financial benefit. Missing a step or rushing the research phase can result in higher management fees or less competitive finance rates.

- Step 1: Financial Discovery. Use a calculator to determine your budget based on your current salary and driving habits. This helps you understand the impact on your take-home pay before committing to a specific car.

- Step 2: Securing Quotes. This is the most critical stage. You should compare market rates rather than settling for the first offer.

- Step 3: Employer Consent. Check your company car policy. Some organisations have preferred providers, but many allow you to bring your own quote if it offers better value.

- Step 4: Vehicle Procurement. Once you have finance pre-approval, you select your car. The leasing company often handles the negotiation to secure fleet pricing, which is typically lower than retail.

- Step 5: Finalisation. You sign the Novation Agreement, and your payroll team integrates the deductions into your next pay cycle.

Phase 1: Research and Quote Comparison

Many employees make the mistake of accepting the “in-house” provider suggested by their HR department without looking elsewhere. These default options often carry higher management fees or less competitive interest rates. Using a novated lease quotes service allows you to benchmark these offers against the wider market. When reviewing a quote, look beyond the monthly payment. Ensure it includes all-inclusive running costs like tyres, servicing, and comprehensive insurance. This transparency is vital for understanding the true Tax Benefits and GST Exemptions available to you. For the 2026-2027 financial year, the maximum GST credit for vehicles is $6,353, which represents a significant upfront saving on the purchase price.

Phase 2: Employer Onboarding and Payroll Integration

Approaching your HR or Payroll manager doesn’t have to be a difficult conversation. Most managers appreciate the no-cost nature of the benefit; it costs the company nothing but provides a significant perk to the employee. The paperwork required from the employer is minimal, usually involving a single signature on the Novation Agreement and a quick update to the payroll software. Once the recurring deduction schedule is set, the process becomes automated. If you’re unsure how to start the conversation, you can request a comparison report to show your employer exactly how the arrangement functions.

Calculating the Savings: Tax Benefits and GST Exemptions

The financial appeal of the novated lease process for employees lies in its ability to unlock savings that are otherwise inaccessible to individual car buyers. The most immediate benefit is the GST exemption on the purchase price. When you lease through this arrangement, you don’t pay the 10% GST on the vehicle’s value, up to the ATO’s maximum credit limit of $6,353 for the 2026-2027 financial year. For a $50,000 car, this represents an upfront saving of approximately $4,545, effectively lowering the amount you need to finance from day one.

These savings extend far beyond the showroom floor. Because the leasing company claims GST credits on your behalf, you also save 10% on almost every running cost. Fuel, tyres, servicing, and even car washes are paid for using GST-exclusive funds. When combined with the reduction in your taxable income, the cumulative effect is substantial. By paying for these expenses from your pre-tax salary, you lower your gross income, which can potentially drop you into a lower tax bracket and increase your fortnightly take-home pay. For a detailed breakdown of how these arrangements fit into broader financial planning, Understanding the Three-Way Agreement through government resources can provide additional clarity on salary packaging mechanics.

The EV Advantage: Zero FBT in 2026

In 2026, electric vehicles (EVs) and eligible plug-in hybrids remain the most tax-effective options due to the federal FBT exemption. Provided the vehicle’s value at first retail sale is below the luxury car tax threshold for fuel-efficient vehicles ($91,661 for the 2026-2027 year), it is exempt from the 47% Fringe Benefits Tax. This exemption can save an employee between $8,000 and $15,000 per year compared to a traditional petrol vehicle. Furthermore, the ATO has confirmed an EV home charging rate of 5.47 cents per kilometre for FBT calculations, allowing you to package your home electricity costs as part of your lease.

Pre-Tax vs Post-Tax: The Employee Contribution Method

For those choosing internal combustion engine (ICE) vehicles, the Employee Contribution Method (ECM) is a vital strategy. Since these cars aren’t FBT-exempt, you would normally face a tax liability. By paying a portion of your running costs from your post-tax salary, you “offset” the fringe benefit value, reducing the FBT payable to zero. This “sweet spot” ensures you maximise pre-tax savings without being penalised by the 47% FBT rate.

| Feature | Standard Car Loan ($50k Car) | Novated Lease ($50k Car) |

|---|---|---|

| GST on Purchase | Paid in full ($4,545) | $0 (Saved upfront) |

| Repayment Source | 100% Post-tax salary | Mix of Pre and Post-tax |

| Running Costs | Paid with after-tax dollars | Paid GST-free via salary packaging |

| Taxable Income | No change | Reduced by lease payments |

If you are still weighing up your financing options, our detailed guide on the novated lease vs car loan comparison breaks down exactly how salary packaging stacks up against a traditional lender in 2026, including the full impact on your taxable income and total cost of ownership.

Managing Your Lease: Maintenance, Fuel, and Job Changes

A significant advantage of the novated lease process for employees is the transition to a fully maintained model of car ownership. This arrangement removes the financial spikes associated with vehicle upkeep. Instead of paying for a major service or a new set of tyres out of your savings, these costs are budgeted for and covered by the funds held in your lease account. You are typically issued a fuel card that works at most Australian service stations, ensuring you never pay for petrol with after-tax dollars at the pump.

Administrative tasks are equally streamlined. When your vehicle requires maintenance, you simply take it to an authorised provider. The mechanic contacts the leasing company directly to confirm the work matches your service schedule and settles the bill from your pre-allocated funds. Regarding kilometres, most employees in 2026 utilise the statutory method for FBT, which removes the requirement for a physical logbook. However, you should still track your odometer readings to ensure your budget remains accurate for your actual driving habits and to avoid any end-of-year reconciliations.

The residual value, or balloon payment, is a critical factor to understand before your term concludes. The ATO sets specific minimum percentages based on the lease duration to ensure the arrangement remains compliant. For a three-year lease, the residual is set at 46.88%, while a five-year lease drops to 28.13%. This amount is not included in your monthly payroll deductions; it is a final lump sum required to take full ownership of the vehicle at the end of the agreement.

What Happens if You Change Jobs?

One of the most common misconceptions is that a lease ends if you resign. In reality, the lease is portable. During your notice period, you should inform your leasing company of your move. They will provide the necessary paperwork to de-novate the vehicle from your current employer and re-novate it with your new one. If your new employer does not offer salary packaging, you can continue making the lease payments directly from your bank account, though you will lose the pre-tax benefits until you join a participating company.

End-of-Lease Options: Upgrade, Refinance, or Buy Out

As you approach the end of your term, you have three primary paths. You can pay the residual value to own the car outright, often using the tax-free savings you have accumulated over the lease term. Alternatively, many employees choose to trade in the vehicle. If the car is worth more than the residual amount, you can use that profit as a deposit for your next lease. Finally, you can refinance the residual amount for another term, which is a smart way to keep the car while maintaining your salary packaging benefits. To see how these management features fit your budget, you can compare novated lease quotes today.

Why Comparing Novated Lease Quotes is Your Best First Step

The novated lease process for employees is not a take-it-or-leave-it proposition. Many corporate salary packaging programmes rely on a single “in-house” provider, which can lead to complacency in pricing and service levels. Accepting the first quote offered by your HR department without external benchmarking is a common financial oversight. By seeking multiple offers, you gain the leverage needed to ensure the interest rates and management fees are competitive with the current 2026 market standards.

Transparency in interest rates is the most effective way to save thousands of dollars over the life of your lease. With the RBA cash rate stabilised at 4.35% as of June 2026, you should expect finance offers to reflect this stability. However, some providers may inflate the base rate with hidden margins. Seeing three or four different offers side-by-side allows you to identify which financiers are offering genuine value and which are padding their profits. Using an online comparison tool empowers you to enter negotiations with data, ensuring you aren’t overpaying for the convenience of a workplace recommendation.

Avoiding Hidden Fees in the Setup Process

While the tax savings are often the headline feature, the fine print can contain procurement charges and document fees that erode your benefit. It is essential to scrutinise the “Management Fee” charged by the leasing company for administering your account. These fees are typically deducted from your pre-tax salary, but they vary widely between providers. A detailed novated lease quotes comparison is the only reliable way to ensure you aren’t being overcharged for administration. Look for providers who offer a flat, transparent fee structure rather than those who hide costs within the finance rate or vehicle purchase price.

Final Checklist Before Signing Your Agreement

Before you commit to the novated lease process for employees, you must verify the logistical details of your specific vehicle. In 2026, while global supply chains have largely recovered, delivery timelines for popular electric vehicles can still fluctuate. Ensure your quote includes a realistic delivery date to avoid being stuck without a car while payments start. Your final checklist should include:

- Insurance Verification: Confirm the comprehensive insurance policy meets your specific needs and is not just a “one-size-fits-all” product.

- Payroll Approval: Verify that your specific payroll department has approved the leasing provider you have chosen to avoid setup delays.

- Residual Accuracy: Double-check that the residual value matches the ATO’s 2026 statutory percentages for your lease term.

Taking these final precautions ensures that your transition into salary packaging is as efficient and cost-effective as possible.

Maximise Your 2026 Salary Packaging Potential

Securing a new vehicle through salary packaging remains one of the most effective ways to optimise your professional income in 2026. By leveraging GST exemptions on purchase prices and taking advantage of current FBT exemptions for electric vehicles, you can significantly reduce your annual transport expenses. Mastering the novated lease process for employees requires a structured approach, but the long-term financial rewards far outweigh the initial setup effort. You now have the roadmap to navigate employer approvals, manage running costs, and handle job transitions with confidence.

The final step is to ensure you receive the most competitive terms available in the Australian market. Accessing an independent and objective quote comparison is the only way to avoid inflated management fees and uncompetitive interest rates. You can Compare Novated Lease Quotes Now to receive transparent offers from Australia’s leading leasing specialists. Our platform also provides a free 2026 Novated Lease Calculator to help you visualise your exact savings before you commit. Take control of your salary packaging today and don’t leave your potential tax savings to chance.

Frequently Asked Questions

How long does the novated lease setup process take from start to finish?

The setup typically takes between two and four weeks. This timeline depends on how quickly your employer returns the signed novation agreement and the current availability of your chosen vehicle. If you select a car that is already in stock, the finance approval and payroll integration can be finalised within a single pay cycle. However, for certain high-demand electric vehicles in 2026, you should factor in additional time for delivery from the manufacturer.

Can I get a novated lease for a used car or just new vehicles?

You can package a used car provided it meets the financier’s age and condition requirements. Most providers require the vehicle to be no older than 10 to 12 years at the end of the lease term. To maximise your savings, it is best to purchase from a GST-registered dealer, as this allows the leasing company to claim the GST credit on the purchase price. Private sales are possible but often exclude the 10% GST saving.

Is a novated lease still worth it if I do not drive many kilometres?

Yes, a lease is highly beneficial regardless of the distance you travel. Following the 2011 tax reforms, the ATO moved to a flat statutory rate, meaning the tax benefits are no longer tied to high mileage. Even if you only use the car for a short daily commute, the GST savings on running costs and the reduction in your taxable income provide significant value. This is especially true for the novated lease process for employees choosing FBT-exempt electric models.

What is the “Residual Value” and why do I have to pay it at the end?

The residual value is a mandatory lump sum payment required by the ATO to ensure the arrangement remains a valid lease rather than a standard hire purchase. The amount is calculated as a percentage of the original purchase price based on the length of your term. For example, a five-year lease carries a 28.13% residual. You must pay this amount, refinance it, or trade the car in to settle the balance at the end of the term.

Can I include my spouse as a driver on the novated lease insurance?

You can certainly include your spouse or other family members as drivers. The comprehensive insurance policies bundled into these agreements typically cover any licensed driver who has your permission to use the vehicle. This flexibility ensures that the car can serve as a primary family vehicle while still maintaining its status as a salary-packaged benefit. You should always verify the specific “named driver” requirements in your insurance Product Disclosure Statement before finalising the agreement.

What happens if I am made redundant while I have a novated lease?

If your employment ends, the novation agreement is cancelled, and the lease becomes a personal finance obligation. You will be responsible for making the full repayments from your bank account using after-tax dollars. Many employees choose to include redundancy insurance in their lease package, which can cover repayments for a set period while you search for a new role. Once you secure new employment, you can simply re-novate the lease with your new employer.

Do I need to be on a high salary to benefit from a novated lease?

You don’t need to be a top-tier earner to see a benefit, though the savings are greatest for those in higher tax brackets. Generally, anyone earning over $45,000 per year will see a positive impact on their take-home pay. Since the novated lease process for employees allows you to save 10% on the car’s purchase price and all running costs, the GST savings alone often outweigh the costs for those on moderate incomes. If you are currently using a traditional lender and want to understand the full cost difference, reading about the novated lease vs car loan outcomes for moderate-income earners can help you make a more informed decision.

How does the GST saving work on the purchase price of the car?

The financier claims the GST on the vehicle as an Input Tax Credit and passes that saving directly to you. This means you only finance the GST-exclusive price of the car, which effectively reduces your loan amount by up to 10% from the outset. For the 2026-2027 financial year, this saving is capped at $6,353. Because you are borrowing less, your monthly repayments and interest costs are lower than they would be with a standard consumer loan.