Why would you pay the full retail price for a new vehicle when the Australian tax system essentially offers you an immediate 10% discount? For most employees, the sticker price is just a starting point, yet many remain unaware that they can bypass the GST entirely on both the car and its upkeep. Understanding how to maximise your novated lease GST savings is the most direct way to increase your take-home pay while driving the car you actually want in 2026.

It’s understandable if you feel overwhelmed by the choice between pre-tax and post-tax deductions or worry about hidden costs buried in lease quotes. This guide explains exactly how the 1/11th discount applies to your purchase price, up to the 2026-27 GST credit limit of A$6,353, and how those savings extend to every litre of fuel and every logbook service. We will clarify how these benefits work for used cars and private sales, providing you with the clarity needed to use a calculator and model your real-world financial outcome with total confidence.

Key Takeaways

- Learn how to secure an immediate 1/11th discount on your vehicle’s purchase price by bypassing the GST up to the 2026-27 ATO limit of A$6,353.

- Discover how to lower your ongoing running costs by claiming back the GST on fuel, tyres, and servicing through your employer’s Input Tax Credits.

- Master the mechanics of novated lease GST savings to understand exactly how the leasing company passes tax credits from the ATO back to your pocket.

- Understand how the 2026-27 luxury car tax thresholds and depreciation limits affect the maximum amount of GST you can save on premium vehicles.

- Identify the red flags in lease quotes to ensure your provider is transparently passing through the full value of available GST credits.

What are Novated Lease GST Savings?

A novated lease is a strategic financial arrangement that transforms a private vehicle purchase into a business expense for tax purposes. At its core, the primary advantage stems from how the Australian Taxation Office (ATO) treats Goods and Services Tax (GST) for businesses compared to individuals. When you buy a car privately, you pay the full retail price including 10% GST, which is a non-refundable cost. However, under a salary packaging arrangement, your employer uses “Input Tax Credits” (ITCs) to effectively strip that GST out of the equation. This mechanism is what creates novated lease GST savings, allowing you to avoid paying the 10% tax that usually applies to the purchase price and ongoing expenses.

Before diving into the tax credits, understanding What is a Novated Lease? is essential for any professional looking to optimise their salary. It’s a three-way agreement where your employer takes on the lease obligations, pays the financier from your pre-tax income, and claims the GST back from the ATO. Because the leasing company acts as a professional conduit, they can pass 100% of these credits back to you. This is the only legal way for a PAYG employee to “claim back” the GST on a passenger vehicle, a benefit usually reserved for business owners or ABN holders.

The savings are split into two distinct categories. First, there is the immediate reduction in the vehicle’s purchase price. Second, there are the recurring savings on running costs. Every time you pay for fuel, a new set of tyres, or a logbook service through your lease, the 1/11th GST component is credited back to your account. This means your budget stretches significantly further than it would if you were paying with post-tax “pocket money” at the retail pump or service centre.

The 1/11th Discount Explained

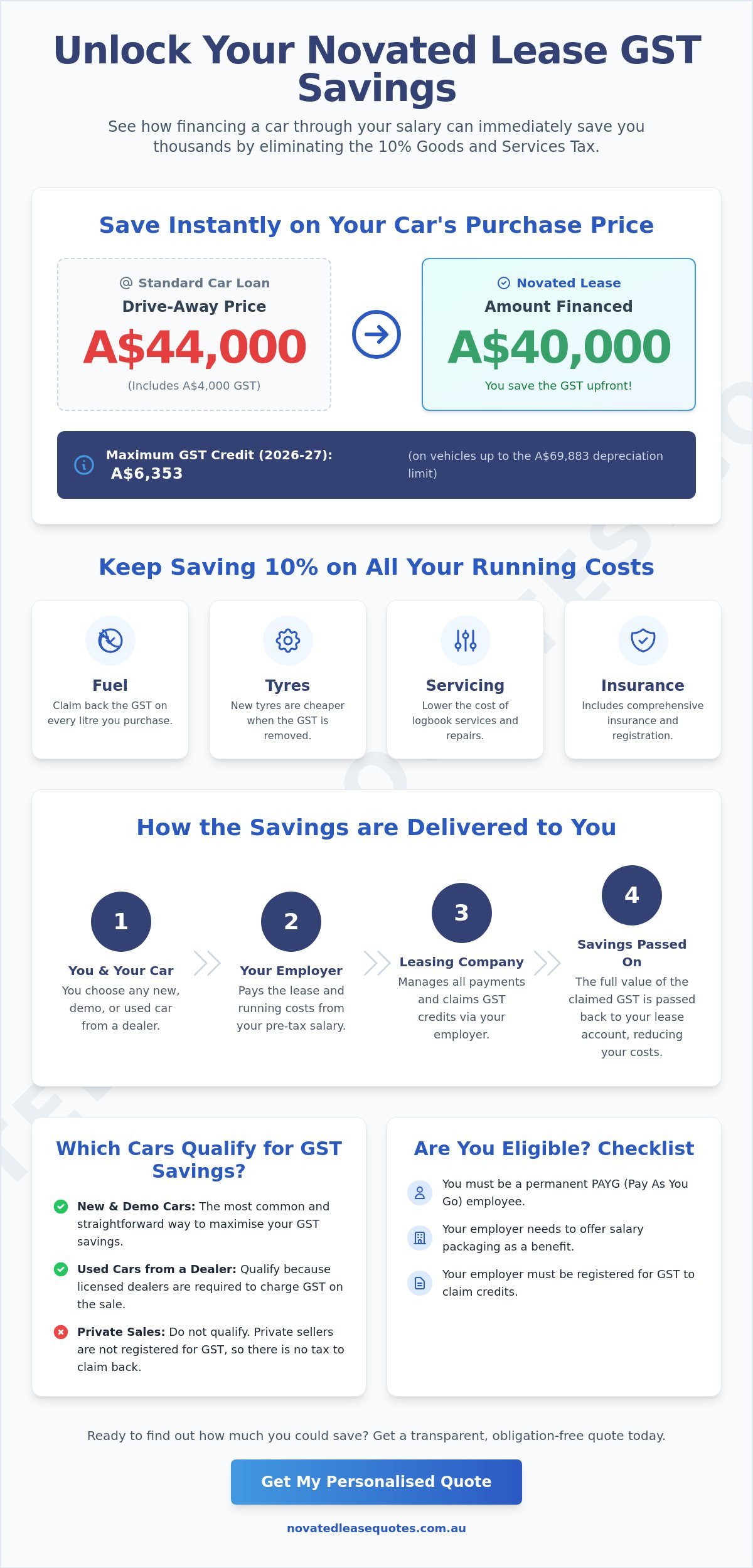

The math behind the discount is straightforward but powerful. To find the GST-free price, the leasing company divides the drive-away retail price by 1.1. If you’re looking at a car priced at A$44,000, the GST component is A$4,000. By eliminating this amount from the start, you only finance A$40,000. This “day-one” saving reduces your total amount financed, which in turn lowers the monthly interest charges you incur over the life of the lease. It’s a compounding benefit that puts you in a much stronger equity position compared to a standard car loan.

Who is Eligible for These Savings?

To access novated lease GST savings, you must be a permanent employee at a company that offers salary packaging. Your employer must be registered for GST, as they are the entity technically “buying” the service and claiming the credits from the ATO. While most private companies and government departments are eligible, it’s vital to confirm your payroll department is set up for the three-way agreement. If your employer isn’t GST-registered, they cannot claim the credits, and the GST savings won’t be available to you.

GST Savings on the Vehicle Purchase Price

When you walk into a dealership, the “drive-away” price you see on the windscreen includes 10% GST. For a standard buyer, this is a sunk cost. However, in a salary packaging arrangement, the leasing company pays the dealer the full amount and then claims the GST back from the ATO as an Input Tax Credit. This creates a financial loop where the GST is stripped out of the transaction before your finance is even established. Because the tax is removed upfront, the amount you actually finance is significantly lower than the retail price, which immediately reduces your monthly interest charges and total loan liability.

The official GST treatment of novated leases ensures that this credit flows directly to the benefit of the employee. For a vehicle with a drive-away price of A$44,000, your novated lease GST savings amount to A$4,000. This means you only finance A$40,000. If you choose a more expensive vehicle priced at A$66,000, the saving increases to A$6,000. It’s vital to note the ATO cap for the 2026-27 financial year; the maximum GST credit you can claim is A$6,353. This limit is tied to the car depreciation limit of A$69,883, meaning any portion of a car’s price above this threshold does not attract further GST credits.

New, Demo, and Used Cars: Do They All Qualify?

New cars and dealership demonstrators are the most straightforward way to access these benefits because they always carry a clear GST component. Used cars purchased through a licensed dealer also qualify, as the dealer is required to charge GST on the sale. You should be wary of the “private sale trap” when buying from an individual. Since most private sellers aren’t GST-registered, there is no GST for the leasing company to claim back. If you buy privately, you effectively forfeit that 10% upfront saving, often making a newer dealer-sourced car cheaper over the life of the lease. To find the best deal on available stock, it’s worth comparing novated lease quotes for both new and used options.

EVs and the GST Advantage in 2026

The synergy between GST credits and the Electric Car Discount is the most powerful tax play currently available to Australian professionals. In May 2026, electric vehicles hit a record 20% market share, largely because of how these incentives stack together. The FBT exemption for eligible electric vehicles continues for the 2026-27 financial year for vehicles priced below the fuel-efficient luxury car tax threshold of A$91,661. By choosing an EV, you save the GST on the purchase price and eliminate Fringe Benefits Tax entirely, representing a double-layered tax saving that internal combustion vehicles cannot match.

Saving GST on Running Costs: The Ongoing Benefit

The financial advantage of a novated lease extends far beyond the initial purchase. While the upfront discount is substantial, the long-term impact on your household budget comes from the novated lease GST savings applied to your day-to-day running costs. When you pay for car expenses with your post-tax “pocket money”, you’re paying the full retail price, which includes 10% GST. Through a lease, your employer claims this GST back as an Input Tax Credit and passes the saving directly to your lease account.

This “Gross vs Net” cost difference means your salary effectively gains 10% more purchasing power for every car-related expense. According to the Australian Taxation Office guidelines on GST, businesses can claim credits for the GST included in the price of things they buy for their business. In a novated lease, your car is treated as a business-related expense for your employer, allowing them to strip the GST from your fuel, maintenance, and insurance bills before the money leaves your pay packet. To understand the full scope of expenses you can package and how each one generates a GST saving, a comprehensive guide to novated lease running costs will walk you through every eligible category in detail.

Managing these costs through a single, bundled payment also adds a layer of professional efficiency to your personal finances. Instead of tracking individual receipts and worrying about price fluctuations, your lease budget is calculated to cover all expected outgoings at their GST-free rate. This ensures your cash flow remains predictable and your tax benefits are maximised without any administrative burden on your end.

Fuel, Tyres, and Servicing

Every time you fill up at the pump or charge your EV, you’re usually paying a 1/11th tax to the government. With a lease, that 10% stays in your pocket. This cumulative effect is significant; over a typical five-year lease, these small savings on petrol or electricity, tyres, and logbook servicing can add thousands of dollars back to your bottom line. It’s a highly efficient way to manage a depreciating asset because it ensures you never pay more than the wholesale, GST-free cost for upkeep.

Insurance and Registration

Comprehensive car insurance premiums always include a GST component, which is fully claimable through your lease. This makes your annual premium 10% cheaper than if you paid the insurer directly. It’s worth noting that while registration and Compulsory Third Party (CTP) insurance are bundled into your payments, their GST treatment can vary. Some registration fees are considered a tax and don’t carry GST, but having a specialist provider manage these ensures you’re always capturing every possible cent of novated lease GST savings without having to track receipts yourself.

The GST Cap and Luxury Car Limits for 2026

While the benefits of novated lease GST savings are extensive, they aren’t unlimited. The ATO imposes a ceiling on the amount of Input Tax Credit (ITC) an employer can claim for a passenger vehicle. This limit is fundamentally tied to the “car limit” or “depreciable limit,” which is updated annually to reflect market conditions. For the 2026-27 financial year, this limit is set at A$69,883. If your chosen vehicle costs more than this amount, your GST savings won’t continue to climb; they hit a hard plateau at the maximum claimable threshold.

The maximum GST credit claimable for a vehicle in the 2026-27 financial year is A$6,353. This figure represents exactly 1/11th of the A$69,883 car limit. Any portion of the vehicle’s price exceeding this depreciable limit is considered “GST-heavy” because you cannot claim the tax back on the excess. Consequently, the most tax-efficient vehicles are often those priced just under this threshold, as they allow you to capture the full 10% discount on the entire purchase price before the cap applies.

Luxury Car Tax (LCT) vs GST

It’s vital to distinguish between GST and Luxury Car Tax (LCT), as they operate in opposite directions. While GST is a tax you aim to save, LCT is an additional tax applied to vehicles above specific price points. For the 2026-27 period, the LCT threshold for fuel-efficient vehicles, including most electric models, is A$91,661. For all other vehicles, the threshold is significantly lower at A$80,809. Unlike GST, there is no mechanism to “claim back” LCT through salary packaging. High-end electric vehicles enjoy a distinct advantage here, as their higher threshold allows you to spend more on the car before the extra tax burden begins to erode your overall savings.

Calculating the “Real” Saving on High-Value Cars

When comparing a A$60,000 car to a A$90,000 car, the financial dynamics shift. On the A$60,000 vehicle, you save the full A$5,454 in GST. However, on the A$90,000 vehicle, your saving is strictly capped at the A$6,353 maximum. This means that as the car price rises above the depreciable limit, the “effective” discount percentage drops. To understand how these caps interact with your specific salary and car choice, it’s essential to request detailed novated lease quotes that break down the exact ITC pass-through. The maximum GST credit you can claim on a novated lease for the 2026-27 financial year is capped at A$6,353.

Maximising Your Savings: How to Compare Quotes

The monthly payment figure on a quote is often the first thing people look at, but it doesn’t tell the whole story. A quote that appears marginally cheaper might actually be less efficient if the provider isn’t passing through 100% of the Input Tax Credits. To truly capture the maximum novated lease GST savings, you need to scrutinise the breakdown of how GST is handled on both the purchase price and the budgeted running costs. Transparency is the hallmark of a professional leasing partner; any ambiguity in how tax credits are applied should be a red flag. Learning how to compare novated lease quotes on a line-by-line basis is the most effective way to ensure you’re capturing every available GST credit rather than being misled by a low headline repayment figure.

Using a Novated Lease Calculator allows you to model different scenarios, such as varying lease terms or car prices, to see how the GST cap affects your bottom line. Since the maximum GST credit is A$6,353 for the 2026-27 financial year, a calculator helps you identify the financial sweet spot. This is where you maximise your tax benefits without hitting the diminishing returns of the luxury car tax threshold. Comparing multiple providers is the only way to ensure you aren’t leaving money on the table through hidden margins or inefficient procurement.

What to Look for in a Novated Lease Quote

When reviewing your documentation, look specifically for the “GST Credit” line item. This should clearly show the 1/11th reduction in the vehicle’s purchase price. Beyond the upfront savings, check that the residual value, or balloon payment, aligns with the current ATO minimum guidelines. For 2026, these mandatory minimums are:

- 1-year lease: 65.63%

- 3-year lease: 46.88%

- 5-year lease: 28.13%

Management fees are a standard part of the service, but they must be weighed against the total tax savings generated. A slightly higher fee from a provider who secures better fleet pricing and manages every ITC claim meticulously is often better value than a budget provider with poor administrative oversight. Always ensure the novated lease GST savings on your running costs are being credited back to your account monthly rather than annually.

Using the Novated Lease Quotes Comparison Service

Professional guidance is invaluable when navigating the interaction between GST credits and FBT implications, especially with the record 20% market share of EVs in 2026. Novated Lease Quotes simplifies this complex marketplace by providing clear, side-by-side comparisons of the leading providers in Australia. This service ensures that the quotes you receive are transparent, competitive, and tailored to your specific salary bracket and vehicle preferences. Don’t settle for the first quote your employer’s default provider offers. Get your competitive novated lease quotes today and ensure you are capturing every cent of available tax relief.

Secure Your 2026 Tax Advantages Today

Maximising your novated lease GST savings is about more than just the initial purchase price. It requires a comprehensive approach that captures every available credit on fuel, maintenance, and insurance throughout your lease term. By understanding the 2026-27 GST cap of A$6,353 and leveraging the current FBT exemption for electric vehicles, you can significantly reduce the total cost of ownership compared to traditional finance. These layered benefits ensure your salary goes further while you drive a newer, safer vehicle.

Accessing these benefits is simple when you have the right data at your fingertips. You can Compare Novated Lease Quotes and Maximise Your GST Savings through our professional platform. We provide direct access to Australia’s leading lease providers, a free Novated Lease Calculator for 2026 tax modelling, and expert guidance on the latest GST and FBT exemptions. Take control of your salary packaging today and drive a better deal for your financial future.

Frequently Asked Questions

Do I really save 10% on the purchase price of the car?

Yes, you save the full GST component, which is 1/11th of the total drive-away price. This discount applies immediately because the leasing company claims an Input Tax Credit from the ATO and passes the benefit to you. It effectively reduces the amount you finance from day one, which also lowers the total interest you pay over the life of the agreement.

Is there a limit to the GST savings on a novated lease in 2026?

The maximum GST credit you can claim for the 2026-27 financial year is A$6,353. This cap is strictly linked to the ATO car depreciation limit of A$69,883. While you can still lease a vehicle priced above this amount, you won’t receive additional novated lease GST savings on the portion of the purchase price that exceeds this threshold.

Can I save GST on a used car bought from a private seller?

No, you cannot save the GST on a private sale because most individuals aren’t GST-registered entities. To access the 10% upfront saving, you must purchase the vehicle through a licensed motor vehicle dealer. This is a common trap for buyers; a “cheaper” private car often ends up costing more over the lease term once the lost GST credit is factored in.

What happens to the GST savings if I leave my job?

If you leave your employer, the lease is “de-novated” and becomes a standard finance agreement. You’ll lose the ability to pay from your pre-tax salary and the associated GST credits on running costs until you start with a new employer who agrees to the novation. Most professionals find a new role and simply transfer the lease to maintain their novated lease GST savings.

Do GST savings apply to electric vehicle charging costs?

Yes, GST savings apply to all eligible EV charging expenses included in your salary packaging budget. Whether you use public charging networks or a dedicated home charger provided through the lease, the 1/11th GST component is claimed back by your employer. This further enhances the financial benefits of the FBT exemption for eligible electric vehicles in 2026.

Why does my lease quote show GST on the payments if I am supposed to be saving it?

Finance providers are legally required to charge GST on lease rentals, which is why it appears on your quote. However, because your employer is GST-registered, they claim this amount back from the ATO as an Input Tax Credit. The “net” cost deducted from your salary is the GST-free amount, ensuring you aren’t actually paying the tax from your take-home pay.

Are the GST savings different for high-income earners?

The GST saving itself is a flat 1/11th discount regardless of what you earn. However, the overall effectiveness of the lease is higher for those in higher tax brackets. While everyone avoids the GST on fuel and servicing, high-income earners also see a larger reduction in their taxable income, providing a greater total tax benefit than those on lower salaries.

Does the GST saving apply to the balloon payment at the end of the lease?

No, the GST saving does not apply to the final residual or balloon payment. When you pay out the lease at the end of the term to own the vehicle, you are required to pay GST on that final amount. This is an ATO requirement and is a key reason why many drivers choose to trade in their car for a new lease rather than paying out the residual.