With battery electric vehicles accounting for a record 20% of all new car sales in May 2026, the shift toward sustainable driving is no longer a future trend; it’s the current standard for Australian professionals. You likely recognise that an ev novated lease fbt exemption is the most powerful tool available to reduce your taxable income, yet the constant updates to ATO rules and Luxury Car Tax thresholds can make the process feel unnecessarily complex. We understand the frustration of trying to track changing PHEV eligibility or worrying about how a new car might increase your HECS or HELP debt repayments.

This guide simplifies the mechanics of salary packaging to help you capitalise on the current $91,387 threshold before the Federal Government’s scheduled phase-out begins in April 2027. We will show you exactly how to model your potential savings using an EV novated lease calculator, allowing you to compare models and secure a lower monthly car cost with total confidence. By the end of this article, you’ll have a clear roadmap to navigate the 2026 tax landscape and lock in your savings while the full exemption remains in place.

Key Takeaways

- Learn how the ev novated lease fbt exemption eliminates the 20% statutory formula tax, significantly increasing your monthly take-home pay compared to a standard car lease.

- Discover the specific 2026/2027 Luxury Car Tax threshold that determines whether your chosen electric vehicle qualifies for the full Federal Government exemption.

- Identify how the GST advantage allows you to save 10% on both the initial vehicle purchase price and all ongoing running costs, from charging to maintenance.

- Understand the mechanics of the Reportable Fringe Benefit Amount (RFBA) and how it may impact your HECS or HELP debt repayments and other income-tested obligations.

- Learn why a standard lease calculator is insufficient for electric vehicles and how to use a specialised tool to model your specific 2026 salary packaging savings.

Understanding the EV Novated Lease FBT Exemption in 2026

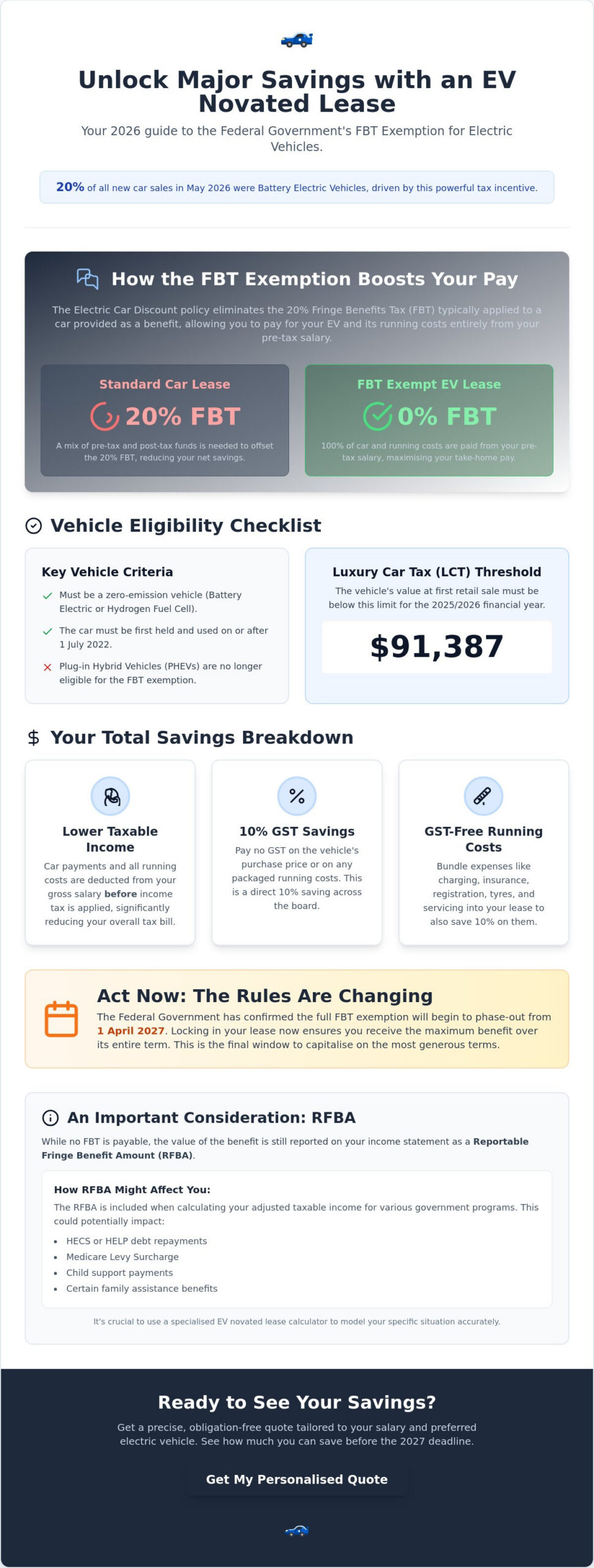

The Federal Government’s Electric Car Discount policy has fundamentally shifted the economics of vehicle ownership in Australia. By May 2026, battery electric vehicles (BEVs) reached a record 20% of all new car sales, proving that the ev novated lease fbt exemption is no longer a niche incentive for early adopters. It’s a mainstream financial strategy. This policy removes the 20% statutory formula tax usually applied to car fringe benefits, provided the vehicle sits below the Luxury Car Tax (LCT) threshold. For the 2025/2026 financial year, this threshold is set at $91,387. By eliminating this tax, the government has made it possible for a premium electric SUV to cost less per month than a mid-range petrol equivalent.

Why 2026 is a Pivotal Year for EV Leasing

Timing is everything in tax planning. The May 2026 budget confirmed that the full FBT exemption will begin a phase-out period from 1 April 2027. This makes the current year the final window to lock in a multi-year lease under the most generous terms. Market maturity has also reached a tipping point. There are now more electric models available under the $91,387 threshold than at any other time in Australian history. We’ve moved beyond limited hatchbacks to a diverse range of family SUVs and performance sedans. This increased competition, combined with the looming 2027 changes, has created a high-demand environment for professionals looking to optimise their salary packaging before the rules tighten.

The Core Mechanism: Pre-Tax Salary Packaging

To appreciate the savings, you first need a solid foundation in Understanding Novated Leases and how they interact with the ATO. In a standard petrol lease, you typically use a combination of pre-tax and post-tax income to offset Fringe Benefits Tax. This is known as the Employee Contribution Method. However, an ev novated lease fbt exemption allows you to pay 100% of your lease costs and running expenses entirely from your gross salary.

This mechanism creates several immediate advantages:

- Gross Salary Deduction: Repayments are taken before income tax is calculated, effectively lowering your taxable income.

- GST Savings: You don’t pay GST on the purchase price of the car or its ongoing running costs, such as tyres and charging.

- Zero FBT: The employer avoids the liability of providing a car benefit, a saving they pass directly to you.

Employers are increasingly encouraging this transition. It helps them meet corporate ESG (Environmental, Social, and Governance) goals while offering a high-value benefit that doesn’t increase their payroll tax burden. It’s a rare scenario where government policy, environmental targets, and personal financial gain align perfectly.

Eligibility Criteria: Does Your Vehicle Qualify for the Exemption?

Securing an ev novated lease fbt exemption requires more than just picking a car with a plug. The ATO maintains strict definitions regarding which vehicles qualify for the Electric Car Discount. Primarily, the vehicle must be a zero-emission car, which includes Battery Electric Vehicles (BEVs) and Hydrogen Fuel Cell Electric Vehicles. There is also a temporal requirement; the car must have been first held and used on or after 1 July 2022. This means that if you are considering a used vehicle, you must verify its original registration date to ensure the tax benefits remain intact.

The exemption extends beyond the car’s finance. It also covers associated running costs, provided they are packaged within the lease. These typically include:

- Registration and CTP insurance

- Comprehensive vehicle insurance

- Scheduled servicing and general maintenance

- Tyres and roadside assistance

- Electricity for charging the vehicle

Understanding how the FBT exemption reduces EV costs across these operational expenses is vital for calculating your total cost of ownership. If you aren’t sure if your preferred model fits these criteria, obtaining novated lease quotes can provide immediate clarity on specific vehicle eligibility.

The PHEV Sunset: What You Need to Know

A common point of confusion in 2026 involves Plug-in Hybrid Vehicles (PHEVs). As of 1 April 2025, the Federal Government removed PHEVs from the FBT-exempt list for all new lease agreements. If you already have a PHEV lease that commenced before this date, your exemption generally continues until the end of that specific lease term. For everyone else, BEVs are now the only practical path for maximising tax optimisation. The shift reflects a policy move toward pure electric transport, making petrol-assisted hybrids a less fiscally attractive option for salary packaging.

Navigating the Luxury Car Tax Threshold

The Luxury Car Tax (LCT) threshold acts as a hard ceiling for FBT eligibility. For the 2025/2026 financial year, the threshold for fuel-efficient vehicles is $91,387. This figure increases slightly to $91,661 for the 2026/2027 financial year. If the retail price of your EV exceeds this limit, even by a single dollar, the entire ev novated lease fbt exemption is forfeited.

You must be cautious with optional extras. High-end paint, panoramic sunroofs, or performance wheel upgrades are included in the LCT value calculation. To stay under the limit while choosing a high-spec model, focus on vehicles where the base price leaves enough room for your preferred accessories. Smart buyers often opt for models that include premium features as standard equipment within the base price to avoid accidentally crossing the threshold.

Quantifying the Savings: FBT Exempt vs. Standard Leases

The financial advantage of an ev novated lease fbt exemption becomes most apparent when you compare the monthly cash flow of a petrol vehicle against an electric equivalent. Consider a $60,000 petrol SUV versus a $65,000 electric SUV. Under a standard lease, the petrol car requires a combination of pre-tax and post-tax payments to manage the Fringe Benefits Tax liability. In contrast, the electric SUV allows for 100% pre-tax deductions. Despite the higher sticker price, the electric model often results in significantly higher take-home pay. This is because the ATO guidelines on the EV FBT exemption remove the 20% statutory formula tax, effectively subsidising the premium cost of the battery technology.

GST Savings on Purchase and Running Costs

The savings begin before you even drive out of the dealership. When you package an EV, the leasing company claims the GST on the purchase price, which can reduce your financed amount by up to several thousand dollars. This 10% discount applies to almost every aspect of vehicle ownership. You don’t pay GST on tyres, insurance, or scheduled maintenance. Charging costs are also included in this tax-free umbrella. Whether you use public fast-chargers or package your home electricity costs, you are paying with pre-tax dollars. Because electric motors have fewer moving parts than internal combustion engines, your maintenance spend is lower from the start, further improving the Total Cost of Ownership over a three-year term.

Income Tax Bracket Optimisation

Your marginal tax rate is the primary driver of your total savings. While the exemption benefits all eligible employees, those in the 30%, 37%, or 45% tax brackets see the most dramatic results. By deducting the lease payments from your gross salary, you reduce your total taxable income. This can sometimes even pull your remaining income into a lower tax bracket.

The “sweet spot” for many Australians is the 37% bracket, where the combination of income tax savings and the FBT removal creates a massive fiscal delta compared to buying a car with post-tax savings. It is essential to model your specific scenario to understand the exact impact on your bank balance. You can use an ev novated lease calculator to input your gross salary and compare different EV models. This data-driven approach ensures you select a vehicle that maximises your disposable income while staying within the 2026 LCT thresholds.

The Reportable Fringe Benefit (RFBA) Reality Check

One of the most common misconceptions regarding the ev novated lease fbt exemption is that “FBT-exempt” means the benefit is invisible to the tax office. While it’s true that neither you nor your employer pays the 47% Fringe Benefits Tax, the value of the benefit must still be reported. If the taxable value of your car benefit exceeds $2,000 in a fringe benefits tax year, your employer is required to record the grossed-up taxable value on your payment summary. This is known as the Reportable Fringe Benefit Amount (RFBA).

The calculation is straightforward but carries significant weight. The ATO uses a statutory gross-up rate of 1.8868. For an electric vehicle, the taxable value is generally calculated as 20% of the car’s cost. For example, a $60,000 EV would have a taxable value of $12,000, resulting in an RFBA of approximately $22,641. While this amount is not included in your taxable income for income tax purposes, it is used to determine your “adjusted taxable income” for various government obligations and benefits.

Managing HECS/HELP and Child Support

If you have an outstanding HECS or HELP debt, the RFBA is the most critical factor to model before signing a lease. Because your compulsory repayments are based on your adjusted taxable income, the addition of a reportable benefit can push you into a higher repayment tier. While this means you are paying off your student debt faster, it does impact your monthly cash flow. Most employees find that the substantial income tax savings provided by the ev novated lease fbt exemption far outweigh the increase in debt repayments. However, you should always calculate the net effect on your take-home pay to avoid surprises at tax time.

Medicare Levy Surcharge (MLS) Considerations

High-income earners who do not have private hospital cover must be wary of the Medicare Levy Surcharge tiers. The RFBA can potentially push your adjusted income into a higher MLS bracket, increasing your tax liability by 1% to 1.5% of your total income. If you are close to a threshold, this could negate a portion of your lease savings. To navigate these complexities, consulting with a novated lease specialist australia is essential for a tailored assessment of your financial position. To ensure you aren’t caught out by tier changes, it’s wise to request a detailed quote comparison that factors in your specific income level and debt obligations.

Using an EV Novated Lease Calculator to Plan Your 2026 Upgrade

Relying on a generic car loan or lease calculator is a common mistake that leads to inaccurate financial expectations. Most standard tools are designed for petrol vehicles; they automatically apply post-tax contributions to offset Fringe Benefits Tax. Because the ev novated lease fbt exemption allows for 100% pre-tax payments, these legacy calculators will significantly underestimate your actual take-home pay. A specialised tool is required to correctly model the zero-FBT environment and the GST credits available on both the vehicle price and its running costs.

To get a precise result, you need three primary data points: your gross annual salary, your estimated annual kilometres, and the vehicle’s drive-away price. The calculator uses your salary to determine your marginal tax rate, which dictates the “discount” you receive on every dollar spent on the car. This level of detail allows you to perform a meaningful side-by-side comparison of different brands. For instance, comparing a Tesla vs BYD can reveal how different price points and residual values impact your weekly budget, even if both cars sit below the LCT threshold.

Modelling Running Costs and Residual Values

The true value of an EV lease isn’t just in the tax break; it’s in the operational savings. Your calculator should allow you to estimate charging costs, which are typically significantly lower than petrol expenses. In the 2026 market, residual values, which is the balloon payment at the end of the lease, are performing differently than in previous years as the second-hand EV market matures. A higher residual value lowers your monthly repayments but leaves a larger amount to pay at the end. Conversely, a lower residual increases your monthly costs but builds more equity in the vehicle. Striking the right balance is key to ensuring the ev novated lease fbt exemption serves your long-term financial goals without creating a cash flow burden.

Getting Multiple Quotes to Ensure the Best Deal

Many employees simply accept the first quote provided by their company’s preferred leasing partner. This can be a costly error. Default providers often include hidden administration fees or higher interest rates that can erode your tax savings. You are generally not obligated to use a specific provider. By using our novated lease quote comparison service, you can verify that the finance and management fees are competitive. This transparency ensures that the thousands of dollars you save through government incentives stay in your pocket rather than being absorbed by service fees. Taking the time to compare ensures your 2026 upgrade is as fiscally responsible as it is sustainable.

Securing Your Electric Future Before the 2027 Phase-Out

The 2026 financial year represents a unique window for Australian professionals to maximise their salary packaging. With the full ev novated lease fbt exemption scheduled to begin its phase-out in April 2027, the time to lock in these significant tax savings is now. By choosing a vehicle under the $91,387 Luxury Car Tax threshold and accounting for your specific RFBA obligations, you can fundamentally lower your cost of living while upgrading to a premium vehicle.

Don’t leave your savings to chance by accepting a single provider’s terms. You can access expert advice on 2026 FBT legislation and use our free-to-use EV savings calculator to model your exact position. Get a Tailored EV Novated Lease Quote and Compare Providers Today to ensure you are receiving the most competitive rates and transparent fee structures available in the market. Our service allows you to compare quotes from Australia’s top leasing specialists at no cost.

Transitioning to an electric vehicle is a smart financial move that aligns your career success with sustainable choices. We are here to help you navigate the technicalities and secure the best possible outcome for your household budget. It’s time to drive a better deal for your future.

Frequently Asked Questions

Is an EV novated lease still worth it if I have a HECS/HELP debt?

An EV novated lease remains financially viable for most employees with a HECS or HELP debt, though your compulsory repayments will likely increase. This occurs because the Reportable Fringe Benefit Amount (RFBA) is added to your adjusted taxable income when the tax office determines your repayment tier. While you will pay off your student loan faster, the significant income tax and GST savings provided by the lease usually far outweigh the impact of the higher repayments.

Can I package a used electric vehicle and still get the FBT exemption?

You can package a used electric vehicle and still qualify for the ev novated lease fbt exemption, provided the car was first held and used on or after 1 July 2022. The vehicle must also meet the other standard criteria, such as being a battery electric vehicle (BEV) and sitting below the Luxury Car Tax threshold. This allows you to combine the lower purchase price of a used model with substantial tax benefits.

What happens to the FBT exemption if I exceed the Luxury Car Tax threshold?

Exceeding the Luxury Car Tax (LCT) threshold by even a small amount results in the total loss of the FBT exemption. For the 2025/2026 financial year, the limit for fuel-efficient vehicles is $91,387. If the vehicle price, including accessories and dealer delivery, goes above this figure, the standard 20% statutory formula tax will apply to the entire lease. This can add thousands of dollars to your annual packaging costs.

Are charging stations and home chargers included in the FBT exemption?

Portable charging cables and public charging costs are included in the ev novated lease fbt exemption, but permanent home charging stations generally are not. The ATO views a wall-mounted home charger as a capital improvement to your property rather than a running cost of the vehicle. You can, however, package the electricity used for charging, provided you use an approved method to calculate the specific energy consumption of the car.

Does the FBT exemption apply to Teslas and high-end EVs in 2026?

The exemption applies to many Tesla models and other high-end EVs in 2026, provided their retail value stays under the $91,387 LCT threshold. Most Model 3 and Model Y variants comfortably qualify. However, premium performance versions or models with extensive optional upgrades may exceed the limit. It’s essential to verify the final drive-away price before finalising your salary packaging agreement.

How does the 1 April 2027 sunset date affect my new EV lease?

The 1 April 2027 sunset date marks the beginning of a phase-out period where the full exemption is reduced for vehicles priced above $75,000. If you secure your lease before this date, your benefits are generally protected for the remainder of your fixed lease term. This makes 2026 a critical year for locking in a three-to-five-year agreement under the most favourable current tax settings.

Can I salary sacrifice an EV if I am a casual employee or on a fixed-term contract?

Salary sacrificing an EV is possible for fixed-term contract employees, but it is often difficult for casual staff due to inconsistent income. Most leasing companies require the contract length to exceed the lease term to ensure repayments are met. You should check your employer’s specific salary packaging policy, as they ultimately decide which employment categories are eligible for a novated lease.

Do I need to keep a logbook for an FBT-exempt electric vehicle lease?

You do not need to maintain a logbook for an FBT-exempt electric vehicle lease. Since the statutory formula tax is completely removed by the exemption, there is no need to prove business versus private use to reduce your tax liability. This significantly simplifies the administration of your lease compared to a standard petrol vehicle where a logbook might be required to lower the FBT.