If you are planning to buy a new car this year, why would you choose to pay for it using income that has already been taxed? It’s a question many professionals overlook, yet failing to consider the “triple-stack” of benefits offered by salary packaging often means leaving thousands of dollars on the table. Understanding your potential novated lease tax savings is the first step toward financial optimisation, especially with the 2026-27 tax brackets and updated Luxury Car Tax thresholds now in effect.

We recognise that the transition from pre-tax to post-tax deductions can feel like a mathematical minefield. You might be concerned that Fringe Benefits Tax will erode your margins or feel uncertain about how the $6,353 GST credit limit applies to your vehicle choice. These are valid concerns that deserve clear, data-driven answers. It’s natural to feel hesitant when the mechanics of take-home pay seem to change with every budget update.

This guide provides a structured approach to estimating your total savings with precision. You’ll learn how to model the impact on your take-home pay and gain the clarity needed to compare a lease against a standard car loan. We will walk through the current FBT exemptions and GST treatments, giving you the confidence to request a quote that aligns with your financial goals.

Key Takeaways

- Master the “triple-stack” of benefits, including GST credits and pre-tax running costs, to reduce your total cost of vehicle ownership.

- Follow a structured framework to estimate your novated lease tax savings using the latest 2026-27 Australian income tax rates and thresholds.

- Maximise your financial position by leveraging the FBT exemption for eligible electric vehicles while the current full incentives remain in place.

- Learn how to scrutinise lease quotes by comparing internal interest rates and management fees instead of just looking at the headline monthly repayment.

- Gain the clarity needed to use a professional calculator so you can accurately compare a novated lease against a standard car loan.

Understanding the Mechanics of Novated Lease Tax Savings

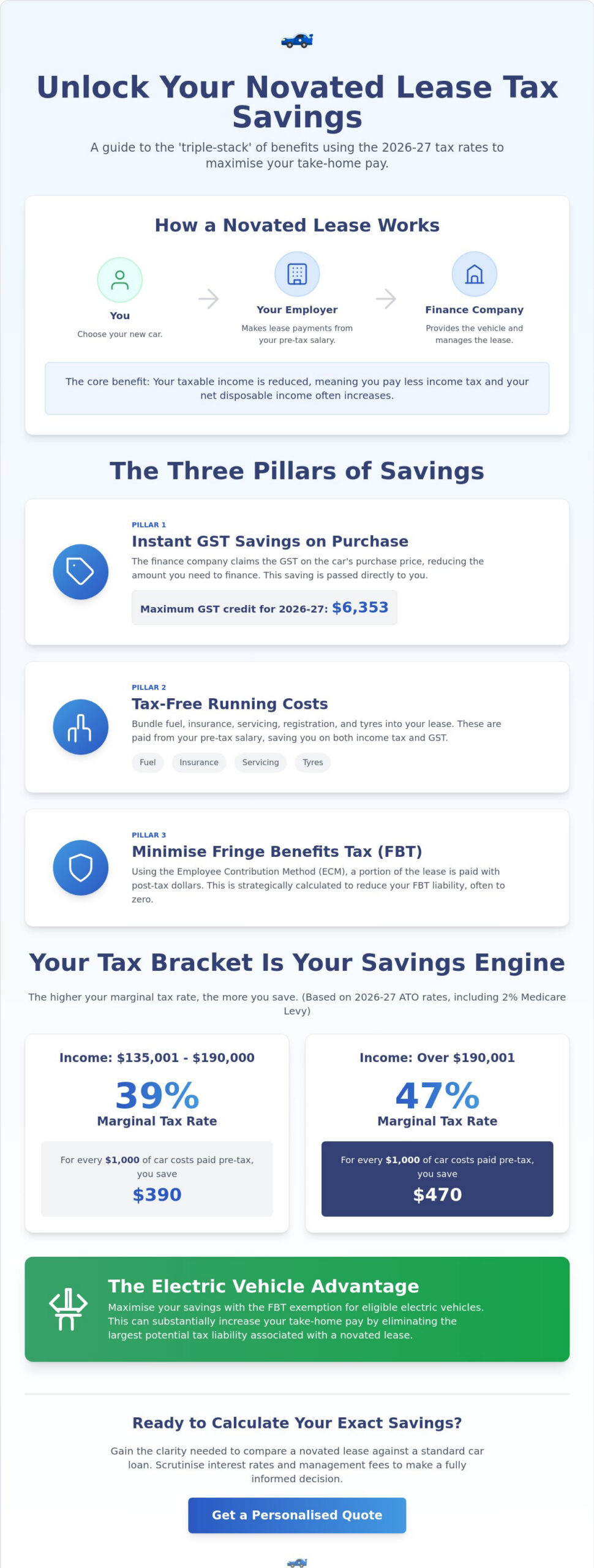

A novated lease is a three-way agreement between you, your employer, and a finance company. It is one of the most effective ways for Australian employees to package their remuneration, effectively turning a standard car loan into a tax-effective salary sacrifice arrangement. To understand What is a novated lease?, it is best to view it as a transfer of lease obligations. Your employer takes on the responsibility for the lease payments, deducting them directly from your salary for the duration of your employment or the lease term.

The primary driver of novated lease tax savings is the reduction of your taxable income. By deducting lease payments and running costs from your salary before tax is applied, you only pay Pay-As-You-Go (PAYG) tax on the remaining balance. The Australian Taxation Office (ATO) allows this because the vehicle is treated as a fringe benefit provided by your employer. While your gross salary decreases on paper, your net disposable income often increases. You are essentially paying for your car’s depreciation and operating costs with “untaxed” dollars that would otherwise have been sent to the tax office.

Pre-Tax vs. Post-Tax Deductions

Pre-tax deductions act as a financial shield for your income. They cover the finance repayments and the majority of your running costs, including fuel, insurance, and servicing. However, many drivers worry about Fringe Benefits Tax (FBT) wiping out these gains. This is managed through a strategy called the Employee Contribution Method (ECM). By making a small portion of your payments from your post-tax salary, you can often reduce the FBT liability to zero. It’s a structured approach that ensures the benefit remains firmly in your favour, providing a clear “tax shield” visible on your annual statement of earnings.

The Role of Your Tax Bracket

Your marginal tax rate determines the strength of your savings. For the 2026-27 financial year, the tax brackets have been adjusted, and identifying where you sit is crucial for accurate calculation. If you earn between $135,001 and $190,000, you fall into the 37% bracket. This means for every $1,000 you sacrifice from your pre-tax pay, you save $370 in income tax, plus the 2% Medicare levy. High earners in the 45% bracket, for those earning over $190,001, find the ultimate “sweet spot” for novated lease tax savings. At this level, nearly half of your car’s running costs are essentially funded by tax savings, making a lease significantly more attractive than a standard consumer loan. If you’re sitting in one of these higher brackets and want to understand precisely how much can I save with novated lease arrangements in 2026, a detailed breakdown of the tax arbitrage mechanics can help you quantify the full advantage.

The Three Pillars of Salary Packaging Tax Benefits

To achieve the highest possible novated lease tax savings, you must understand that the benefit is not a single discount but a combination of three distinct financial pillars. When these pillars are structured correctly, they work in tandem to lower the total cost of ownership far below what is possible with a standard car loan or a cash purchase. This comprehensive benefit stack is what makes salary packaging the preferred choice for savvy Australian professionals.

Instant GST Savings on Purchase

The first pillar provides an immediate advantage before you even drive the car off the lot. When you purchase a vehicle through a novated lease, the financier claims the GST back from the Australian Taxation Office as an input tax credit. This effectively reduces the amount you need to finance by up to 10%. For the 2026-27 financial year, the maximum GST credit you can claim is capped at $6,353. By reducing the principal amount of the lease from day one, you pay less interest over the term of the agreement compared to a standard consumer loan where you would pay the full GST-inclusive price.

Tax-Free Running Costs

The second pillar involves your ongoing “lifestyle expenses” associated with the car. A novated lease allows you to package fuel, tyres, servicing, registration, and insurance into a single, predictable pre-tax payment. You aren’t just saving on income tax here; your employer also passes back the GST input tax credits on these expenses. This means you are effectively paying a GST-free price for your fuel and maintenance. The ATO provides specific guidance on GST and novated leases to ensure these credits are handled correctly. Paying for these costs with tax-free dollars significantly boosts your monthly cash flow.

The Employee Contribution Method (ECM)

The third pillar is a strategic tool used to manage Fringe Benefits Tax (FBT) for internal combustion engine vehicles. FBT is a tax employers pay on benefits provided to employees in place of salary. To prevent this tax from eroding your novated lease tax savings, most leases are organised using the Employee Contribution Method. You pay a portion of your lease costs from your post-tax income, which offsets the FBT liability dollar-for-dollar. This “offset” strategy is the industry standard for maximising efficiency, ensuring you get the tax breaks of salary sacrifice without the sting of additional fringe benefits charges. Requesting a tailored novated lease quote is the most effective way to see these pillars in action for your specific salary and vehicle choice.

How to Estimate Your Personal Tax Savings Step-by-Step

Moving from the theoretical pillars of salary packaging to a practical calculation requires a methodical approach. To accurately project your novated lease tax savings, you must look beyond the monthly repayment and focus on the total impact on your annual cash flow. Many drivers make the mistake of comparing a lease repayment directly to a car loan repayment, which ignores the significant income tax and GST offsets that occur behind the scenes. By following this structured process, you can determine exactly how much extra money remains in your pocket each fortnight.

Step 1: Gathering the Vehicle Data

Your calculation begins with the vehicle’s drive-away price. However, you must strip out the GST component, as the financier claims this back from the ATO. Remember that while the purchase price is GST-exempt, other components like dealer delivery charges and government stamp duty are not, so these must be included in your base figure. The financed amount is the GST-exclusive purchase price of the vehicle plus any non-exempt costs like registration and stamp duty. This lower starting point is the first major advantage of a lease, as you are only paying interest on a reduced principal amount compared to a standard consumer purchase.

Step 2: Using a Professional Calculator

Manual spreadsheets often fail to capture the granular details of Australian tax law. Factors like the 2% Medicare Levy and the specific 2026-27 tax brackets significantly shift the final result. For a precise model that accounts for these variables, you should use our salary packaging car calculator. This tool interprets the “Total Potential Savings” by comparing your current take-home pay against your projected pay after all pre-tax and post-tax lease deductions are processed. It provides a clear view of the “take-home pay effect” that defines the value of the arrangement.

Step 3: Comparing the ‘Net’ Position

The final step is to evaluate your net position over the life of the lease. This means looking at your take-home pay rather than the gross cost of the car. You must also factor in the residual value, often called a balloon payment, which is the ATO-mandated amount you pay to own the car at the end of the term. A professional novated lease tax savings model will also account for corporate discounts. Because lease providers manage large volumes of vehicles, they often secure pricing below what a private buyer can achieve at a dealership. When you combine these purchase discounts with the ongoing tax benefits, the “net” cost of the vehicle is often thousands of dollars less than any other financing method. For a comprehensive breakdown of the precise dollar figures involved, our dedicated guide on how much can I save with novated lease salary packaging walks through each component in detail.

Leveraging the EV FBT Exemption for Maximum Savings in 2026

As of June 2026, the financial landscape for vehicle procurement has shifted decisively in favour of electrification. While the “triple-stack” of benefits discussed earlier applies to all vehicles, electric vehicles (EVs) currently enjoy a unique regulatory advantage that turbo-charges your novated lease tax savings. For an eligible zero or low-emission vehicle, the Fringe Benefits Tax (FBT) is entirely waived, provided the vehicle’s value remains below the luxury car tax threshold. For the 2026-27 financial year, this threshold for fuel-efficient vehicles is set at $91,661. This exemption creates a scenario where you can fund 100% of your lease and running costs from your pre-tax salary without needing to make any post-tax contributions.

Why EVs Change the Calculation

The removal of FBT for eligible EVs fundamentally alters the “take-home pay” equation. When you package a petrol-powered SUV, you must typically use the Employee Contribution Method (ECM) to offset FBT, which involves using some of your post-tax income. With a pure EV, every dollar for the finance, insurance, and maintenance is deducted before a single cent of income tax is calculated. This results in significantly higher savings for the average professional compared to a combustion vehicle of the same purchase price. It is important to note that the rules for Plug-in Hybrids (PHEVs) changed on 1 April 2025. PHEVs are no longer eligible for this specific FBT exemption, making battery electric vehicles the most tax-effective choice in the current market.

Home Charging and Running Costs

Maximising the “green” benefits of your salary package now extends to how you “fuel” the vehicle at home. The ATO has simplified the process for packaging home electricity costs by providing a specific cents per kilometre rate for EV charging. This allows you to claim the cost of charging your car from your own power supply as a pre-tax deduction, further reducing your taxable income. When you combine this with the absence of traditional fuel costs and the lower maintenance requirements of electric drivetrains, the total cost of ownership drops dramatically. You can compare the specific impact of these exemptions on your salary by requesting a tailored novated lease quote to see the 2026 incentives in action.

The current full FBT exemption is scheduled for review by mid-2027, with a gradual phase-out already planned for vehicles priced over $75,000 starting in April 2027. This makes the 2026 financial year a critical window for those looking to lock in the maximum possible novated lease tax savings. By securing a lease now, you ensure your vehicle is treated under the current generous criteria for the duration of your agreement, protecting your financial optimisation from future policy shifts.

Comparing Quotes to Optimise Your Financial Outcome

The structural benefits of salary packaging are significant, but the final value of your novated lease tax savings depends entirely on the quality of the quote you sign. Many employees mistakenly assume that their employer’s preferred leasing provider offers the most competitive terms by default. In reality, these providers often rely on their exclusive access rather than offering the lowest market rates. By comparing multiple offers, you ensure that high interest rates or excessive management fees don’t quietly erode the tax advantages you’ve worked hard to calculate.

It is common for effective interest rates in the novated leasing market to range between 8% and 12% or higher. Even a minor difference in the interest rate can result in thousands of dollars in additional costs over a four or five-year term. Beyond the rate, you must scrutinise the administration fees. These are the monthly charges the leasing company applies to manage your budgets and process payments. If these fees are too high, they can negate a portion of the income tax savings you achieve through salary sacrifice.

What to Look for in a Quote

When reviewing a quote, you must distinguish between the “Base Interest Rate” and the “Effective Interest Rate”. The base rate often excludes the impact of fees and charges, while the effective rate provides a truer picture of the cost of finance. You should also check that the budgets for running costs are realistic. Some providers may under-budget for items like tyres or servicing to make the monthly repayment look lower on paper. This can lead to out-of-pocket expenses later in the lease. Ensure the insurance premiums quoted are competitive and that you aren’t being charged for redundant “add-on” insurance products that provide little actual value.

Securing Your Best Deal

To maximise your financial position, you need to master novated lease quotes by comparing multiple providers simultaneously. Using an independent specialist allows you to negotiate from a position of strength, as they can access a broader range of financiers than a single employer-aligned provider. This competitive approach is the only way to ensure the novated lease tax savings you’ve modelled actually stay in your pocket.

Before you commit to an agreement, ask the specialist about the transparency of their brokerage costs and whether they offer flexibility if your employment circumstances change. A professional consultant will provide a side-by-side comparison that highlights the total cost of ownership, including the residual value. Taking the next step is straightforward. Requesting a tailored quote for your specific car and salary will give you the precise data needed to make an informed, confident decision for the 2026 financial year.

Secure Your Maximum Vehicle Tax Advantage

Our team simplifies this complex marketplace by providing access to multiple Australian leasing providers and offering specialised EV tax advice through an independent quote comparison service. This ensures you aren’t just accepting the first offer, but rather the most competitive one available. Get a Competitive Novated Lease Quote Today to see exactly how much you can save on your next vehicle. Making an informed choice now ensures your salary packaging remains a genuine asset for years to come.

Frequently Asked Questions

Is a novated lease worth it for someone on a low salary?

A novated lease is generally most effective for those in higher tax brackets, but it can still provide value for lower income earners through GST savings. While your income tax reduction is smaller at the 15% bracket, you still avoid paying GST on the vehicle purchase price and ongoing running costs. It is essential to model the specific impact on your take-home pay to ensure the management fees don’t outweigh the benefits.

How much tax will I actually save with a novated lease in 2026?

Your total novated lease tax savings in 2026 depend on your marginal tax rate and the vehicle type. For a professional earning $150,000, saving over $5,000 annually is common for internal combustion vehicles. If you choose an eligible electric vehicle under the $91,661 luxury car tax threshold, these savings can double due to the full FBT exemption. Using a professional calculator is the only way to get a precise figure.

What happens to my tax savings if I change jobs mid-lease?

If you change employers, your lease agreement is portable and can usually be transferred to your new company. This process involves a new “novation” agreement between you and your new employer. If your new workplace doesn’t offer salary packaging, you can continue making payments directly to the financier using post-tax funds. However, the tax benefits will cease until the lease is novated to a participating employer.

Can I save on GST if I buy a used car through a novated lease?

You can save on GST for a used car only if you purchase it through a GST-registered dealership. In this scenario, the financier can claim the GST back, reducing your financed amount. If you buy from a private seller, there is no GST component to claim, which removes one of the primary financial pillars of the lease. Most providers allow used car packaging provided the vehicle meets specific age and condition requirements.

Does a novated lease affect my superannuation contributions?

Most employers calculate Superannuation Guarantee (SG) contributions based on your gross salary before any salary sacrifice deductions. This means your super balance typically remains unaffected by the lease. However, it is vital to confirm this with your payroll department, as some employment contracts specify super is paid on “ordinary time earnings,” which could technically be reduced by packaging. Always review your specific agreement before signing to ensure your long-term retirement goals are protected.

What is the ‘Luxury Car Tax’ and how does it impact my savings?

The Luxury Car Tax (LCT) impacts your savings by capping the amount of GST you can claim back and determining FBT eligibility for EVs. For the 2026-27 financial year, the LCT threshold is $91,661 for fuel-efficient vehicles and $80,809 for others. If your vehicle exceeds these values, you may be liable for LCT, and the GST credit is limited to $6,353. Staying below these thresholds is a key strategy for maximising your overall financial optimisation.

How does the Medicare Levy factor into my novated lease calculation?

The 2% Medicare Levy is calculated on your taxable income, so reducing that income through a lease provides an automatic saving. Because your novated lease tax savings are derived from lowering your gross pay, you effectively pay 2% less on every dollar sacrificed. While it seems like a small percentage, it adds hundreds of dollars to your total annual benefit, especially for those in high-income brackets who are already subject to the levy.

Can I package a car that I already own to get tax savings?

You can package a car you already own through a “sale and leaseback” arrangement. The leasing company purchases the vehicle from you at its current market value and leases it back to you under a novated agreement. This allows you to access the same tax-free running cost benefits and income tax reductions as a new car. It is an efficient way to unlock equity in your current vehicle while reducing your taxable income through salary sacrifice.